Biden’s ESG Agenda

Opposition to “woke” ESG corporatism is snowballing, as Joe Biden and Larry Fink have found out recently. Fink is the billionaire CEO of BlackRock, the world’s largest asset manager, with $8 trillion under management. He is also one of Biden’s biggest boosters and the most prominent corporate promoter of ESG, the controversial rating system that is pushing companies to adopt “progressive” Soros-style policies rather than carry out their legal and fiduciary responsibilities to their shareholders. ESG, which stands for environmental, social, and corporate governance, is a scheme aimed at pressuring businesses into joining the politically correct stampede on climate change, decarbonization, sustainable development, and so-called social-justice and racial-justice issues such as gun control, abortion rights, LGBTQ equity, and critical race theory.

Belated Rally Against ESG Juggernaut

Although ESG has only hit the general public’s radar screens in the past year or so, the ESG program, like most globalist intrigues, has been quietly in the works for decades. (We will return to that important history in a moment.) However, with the dangers of ESG now far more readily apparent, opposition is belatedly forming. Congress is stepping into the breach. State legislatures, governors, and attorneys general are also taking action.

On Tuesday, February 28, the U.S. House of Representatives fired the first salvo aimed at nixing the administration’s ESG program for 401(k) retirement investing, as put forward by the Biden Labor Department’s new rule known as the “Prudence and Loyalty in Selecting Plan Investments and Exercising Shareholder Rights.” The Labor rule, crafted pursuant to President Biden’s “Executive Order on Climate-Related Financial Risk” (EO 14030) of May 20, 2021, was promulgated to undo President Trump’s executive order banning the placing of ESG impositions on pension funds.

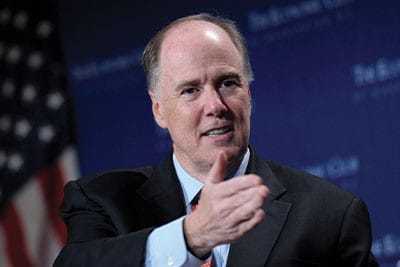

BlackRock blackguard: Billionaire Larry Fink, CEO of BlackRock, which manages more than $8 trillion in assets, has become the leading business face pushing ESG “social credit” controls promoted by the United Nations and the World Economic Forum (WEF).

Speaking on the House floor on February 28, Representative Andy Barr (R-Ky.), the sponsor of the anti-ESG resolution, blasted Democrats for misrepresenting his bill and for failing to protect investors and retirees from the harmful impacts of ESG on their investments. “Nothing in this resolution prohibits an American from allocating their capital the way they want to,” he noted. “But what this resolution will do is stop the Department of Labor from coercing Americans into lower performing, higher fee, less diversified, politicized funds. We must stop the politicization of allocation of capital…. In 2022, the S&P 500 energy sector ended the year a whopping 59 percent higher than where it started, amid a brutal bear market, in which the S&P 500 overall lost 20 percent! If you’re invested in ESG in 2022, you are a massive loser because you are divested from energy. Stop the politicization of capital.”

On an almost straight party-line vote, the anti-ESG measure, House Joint Resolution 30, passed by 216 to 204. Representative Jared Golden of Maine was the sole Democrat to join the Republicans on this vote in the House. The following day, March 1, it passed the Senate by a vote of 50 to 46, with Democratic Senators Jon Tester of Montana and Joe Manchin of West Virginia crossing over to vote with the Republicans.

To dump the ESG rule, Republicans utilized the Congressional Review Act, which lets Congress disapprove — by a simple majority vote — a final rule issued by a federal agency if it has not been in effect for more than 60 legislative days.

On March 20, President Biden used his veto pen for the first time to cancel this legislation and keep his ESG plan in place. Three days later, the House Democrats protected his veto, voting on a straight party-line call to block a GOP effort to override Biden’s veto.

As we have reported here at The New American, more than two dozen states are suing the Biden administration over the ESG rule, and states are divesting from BlackRock, Vanguard, State Street, and other asset managers that are pushing ESG.

Long, Dark History of the ESG Stealth Agenda

The foundation for ESG was laid more than 30 years ago by the Business Council for Sustainable Development (BCSD) at the 1992 Earth Summit. For that United Nations confab in Rio de Janeiro, the BCSD effected a carefully timed release of its book entitled Changing Course: A Global Perspective on Development and the Environment. Accompanied by the scripted hosannahs of the global press, the book introduced much of the world to “responsible investing,” by which was meant a new form of “capitalism” with an enviro-socialist twist. The BCSD, which morphed into the World Business Council for Sustainable Development (WBCSD), has been intimately connected to the Swiss-based World Economic Forum (WEF) led by Klaus Schwab from its inception. The next major step that built on the BCSD foundation came in 1999, when then-UN Secretary-General Kofi Annan went to the WEF’s annual Davos extravaganza to announce the UN’s Global Compact, which was needed, we were told, to promote “responsible business practices and UN values among the global business community.” It claimed the support of thousands of companies, business executives, and “stakeholders” (i.e., paid activists). The following year, 2000, the UN held its Millennium Summit in New York City, which resulted in the UN’s promulgation of its Millennium Development Goals (MDGs).

The MDGs were an attempt to implement piecemeal the UN’s Agenda 21, a massive, 351-page scheme to control all human activity and all the natural resources of the entire planet: oceans, seas, lakes, rivers, streams, swamps, wetlands, mountains, deserts, prairies, tundras, forests, glaciers, air, minerals, energy, farms, rural areas, cities, manufacturing, businesses, schools, healthcare, women’s rights — virtually everything. Unveiled at the Rio Earth Summit, Agenda 21 embodied a totalitarian vision more sweeping than even the communist central planning schemes a Joseph Stalin or Mao Zedong might have imagined. But the difficulty came in how to package, sell, and implement such a colossal and complex program that was so obviously intrusive, abusive, oppressive, and despotic. Thus, the MDGs: a supposedly simplified, digestible program of eight goals, amplified by 18 “targets” and 48 “indicators” — replete with promises to eradicate world hunger, poverty, ignorance, and disease. Voila! Who could resist such wonderful goals? The WEF woke corporatists rushed to sign onto the MDGs, which, we were told, would bring about global nirvana by 2015. But, as we found out, when 2015 came along, the UN-WEF globalists simply upped the ante, replacing the eight Millennium Development Goals with the 17 Sustainable Development Goals (SDGs).

From MDGs to SDGs and ESG

The new SDGs include an associated 169 targets and 232 indicators, all of which would guide humanity to the newly revised global nirvana by 2030. So promised the benevolent one-world technocrats. One such technocrat is Columbia University Professor Jeffrey Sachs, a UN special advisor, George Soros acolyte, WEF agenda contributor, and Council on Foreign Relations (CFR) member. Sachs penned an influential propaganda piece entitled “From Millennium Development Goals to Sustainable Development Goals” for the prestigious British medical journal The Lancet in 2012 to introduce the idea of transitioning from the MDGs to the more detailed SDGs. Thus did the UN’s Agenda 21 (Agenda for the 21st Century) morph into the UN’s current Agenda 2030. And just so that we mere mortals may rest easy knowing that our future is being planned further out, the globalist visionaries already have an Agenda 2050 (also called TWI2050, for The World In 2050) in the works.

There were a couple of additional intermediate steps along the ESG path that deserve mention. What came to be known as ESG — a critical component of the Agenda 21 MDGs and the Agenda 2030 SDGs — began in 2003 at the Geneva-based UN Environmental Program Financial Initiative (UNEP FI) under the leadership of British UN bureaucrat Paul Clements-Hunt and Australian James Gifford, a former enviro-activist with the Wilderness Society. The UNEP FI team led by Gifford and Clements-Hunt developed what has become a network of financial institutions and corporations under the umbrella of the UN Principles for Responsible Investment (UNPRI).

Ginning Up GIIN

The UNPRI, working closely with the WEF and its affiliated corporations, is a prime driver of ESG. The UNPRI website says the organization “is the world’s leading proponent of responsible investment.” The UNPRI works “to understand the investment implications of environmental, social and governance (ESG) factors,” and “to support its international network of investor signatories in incorporating these factors into their investment and ownership decisions.”

UNPRI can now boast an impressive list of hundreds of corporate, institutional, and individual members and supporters, including CEOs and executives from giants such as AG Insurance, Allianz, Alpha Bank, AXA Group, Bank of America, Barclays, BNP Paribas, Carlyle Group, Citigroup, Deutsche Bank, Goldman Sachs, JPMorgan Chase, Lloyd’s of London, and many more.

The process of luring more big-name companies into the ESG web took another important step in 2007, when the Rockefeller Foundation and JPMorgan Chase launched “impact investing” at the foundation’s retreat center in Bellagio, Italy. An outfit called the Rockefeller Impact Investing Collaborative emerged from that gathering. Two years later, in 2009, the Rockefeller Foundation, together with the Annie E. Casey Foundation, W.K. Kellogg Foundation, and JPMorgan Chase Foundation (and corporate allies) launched the Global Impact Investing Network (GIIN), which now includes dozens of major banks, foundations, corporations, funds, and asset managers. “Responsible investing” and “impact investing” have joined ESG, SDGs, and DEI (diversity, equity, and inclusion) as part of the woke lexicon of the new China-style “capitalism” that goes by the names “inclusive capitalism,” “stakeholder capitalism,” and other subversive nostrums pushed by the World Economic Forum and the Council on Foreign Relations and its British counterpart, Chatham House (formally known as the Royal Institute of International Affairs, RIIA).

The BlackRock-Biden Connection

As noted above, the BlackRock behemoth and its CEO Larry Fink are leading promoters of ESG — and globalization. Fink is featured prominently in a video on the WEF website speaking out at the January 2023 WEF summit in Davos against “fragmentation,” which, in globospeak, is a denunciation of those peoples and nations who desire to keep their national sovereignty.

In a video interview with Yahoo!Finance, Fink proudly boasts, “I’m a globalist.” That is no surprise to anyone who has observed the longtime Fink/Blackrock support for the UN SDGs, UN Global Compact, UNPRI, ESG, etc.

Team Biden-BlackRock: Thomas Donilon (CFR), now chairman of BlackRock Investment Institute, was national security advisor to the Obama-Biden administration. His brother Mike Donilon, known as “the Biden Whisperer,” is President Biden’s top advisor. Thomas’ wife, Catherine Russell, served as Jill Biden’s chief of staff. (AP Images)

BlackRock has acquired not only an outsized footprint in the global economy, but also a huge influence in the Biden administration, with former top executives of the firm in key Biden posts and former Obama-Biden officials now rotating into top slots at BlackRock.

Brian Deese, the former global head of sustainable investing at BlackRock and a former senior advisor to President Obama, was named to head Biden’s National Economic Council.

Wally Adeyemo, former chief of staff to Larry Fink at BlackRock and former president of the Obama Foundation, is Biden’s deputy secretary of the treasury under Janet Yellen.

Mike Pyle, a chief investment strategist for BlackRock and an advisor to President Obama and Hillary Clinton, was picked to be Vice President Kamala Harris’ chief economist.

Thomas Donilon, a national security advisor in the Obama-Biden administration, is currently chairman of BlackRock’s research business. Dalia Osman Blass, a former SEC official, is now BlackRock’s chief of external affairs.

BlackRock is also a big player when it comes to political contributions, setting a new record in the 2022 midterm elections.

BlackRock, Vanguard, Goldman Sachs, JPMorgan Chase

BlackRock’s influence on ESG is amplified by other financial titans that have also jumped on the ESG bandwagon, such as Vanguard, State Street, Goldman Sachs, and JPMorgan Chase, to name but a few. We could add corporate giants Google, Apple, Microsoft, Pfizer, PayPal, Salesforce, Hewlett Packard, Deloitte, KMPG, General Motors, and many more.

An important tie these corporate titans have in common is participation in the World Economic Forum, the premier globalist organization that has been promoting ESG for years.

The WEF globalists see ESG as a crucial element of the Great Reset, the plan to “reset” all of humanity politically, economically, socially, biologically, morally, and spiritually.

The WEF is an official “Strategic Partner” of the United Nations, so it should be no surprise that the WEF openly admits that ESG is a system to boost the UN’s 17 Sustainable Development Goals.

As is plainly evident from the WEF’s own website, the Davos globalists want to make ESG the “North Star” guide for all corporations. In a WEF article for January 12, 2023, titled “How to make non-financial reporting your company’s north star,” corporate leaders are told, “Getting ESG right is of crucial importance — not just as a prerequisite for the long-term success of companies. The right approach can bring about a new kind of inclusive capitalism.” After paying homage to “global climate activism, the Me Too or Black Lives Matter movements,” the article goes on to aver, “What’s relevant today is that business serves society. By redefining capitalism, we can build a more just and sustainable world.”

The WEF article then adapts the UN’s icon graphic for the 17 Sustainable Development Goals, dividing them into three groups and placing them under the Environment, Social, and Governance headings.

ESG’s UN genesis: The foundation for ESG was laid more than 30 years ago by the Business Council for Sustainable Development (BCSD) at the United Nations’ 1992 Earth Summit in Rio de Janeiro to implement the UN’s Agenda 21 (which is now Agenda 2030). (AP Images)

If the ESG picture is starting to look a lot like Communist China’s Social Credit System, it’s not an accident. As we have been reporting here for decades, BlackRock, Goldman Sachs, Chase, Citi, and other Wall Street titans have been financing the mass-murdering regime to the tune of hundreds of billions of dollars. These “capitalist” banksters appear to be perfectly at home with China’s communist banksters as fellow members of UNPRI. Among the Chinese Communist Party’s (CCP) “responsible investment” banks at UNPRI are Bank of Beijing, Bank of China, Bank of Huzhou, Bank of Jiangsu, Bank of Jilin, Bank of Jiujiang, Bank of Nanjing, Bank of Suzhou, China Minsheng Bank, Hengfeng Bank, WeBank, and the Industrial and Commercial Bank of China. And anyone who pays attention to the Davos crowd knows that Xi Jinping and other top CCP leaders are treated like rockstars at WEF confabs. Klaus Schwab, the grand poohbah of the Davos billionaire menagerie, has shown repeatedly that he cannot be effusive enough in praising Xi and in welcoming him to the WEF events. In 2022, he honored Xi for China’s “economic and social achievements under your leadership,” completely ignoring Xi’s steel-fisted clampdown throughout China, brutal takeover of Hong Kong, and renewed religious persecution. In business, China has accelerated its National Champions program, in which the CCP has expanded its state-owned enterprises and has much more openly taken control of “private” Chinese companies. Rather than condemning this, the WEF and its corporate members have cheered the CCP’s actions and even adopted its terminology. Since 2007, the WEF has held its Annual Meeting of the New Champions, many of which have taken place in China and which have served to advance the Chinese “Champion” model of state-corporate merger through public-private partnerships, while crushing genuine free-market entrepreneurship. We witnessed this harsh reality during the Covid “pandemic,” which is ongoing, and which has wiped out millions of small and medium-sized businesses worldwide. The Covid lockdowns and mandates that destroyed the mom-and-pop businesses deemed “non-essential” also greatly enriched and enlarged the government-privileged New Champions: Amazon, Walmart, Alphabet/Google, Microsoft, Apple, Zoom, Netflix, Shopify, PayPal, Meta/Facebook, Home Depot, Lowe’s, Costco, JPMorgan Chase, Citigroup, Bank of America, BlackRock, Pfizer, Moderna, Morgan Stanley, Goldman Sachs, and many more — virtually all of which are in bed with China while also cheerleading for the Davos-UN ESG agenda.

While virtue-signaling their ESG scores, the WEF billionaires continue to prop up the Beijing butchers, who have the worst environmental record, commit the most heinous human-rights abuses, run the world’s biggest Orwellian surveillance state/police state, and present an existential threat to America and to freedom worldwide. An anti-ESG group, Consumers’ Research, launched a mobile billboard and digital advertising campaign around the Washington, D.C., area to oppose the expected Biden veto of the congressional legislation. The billboards ask, “What does ESG really stand for?” and suggest that “Elitists Socialists Grifters” and “Erasing Savings Growth” are more apropos.

The Biden veto, along with the “woke” lobby of corporate globalists supporting this push, guarantees that the enormous perils presented by ESG will be with us for the foreseeable future. The battle lines are drawn. Much of the fight now must be taken to the state, local, and individual level, with officials and individual investors refusing to allow the ESG elitists to manage our pensions and investments.